Hey friends, hello! I am Subodh, a guy from Varanasi, who goes through the small financial ups and downs of life every day. These days, there is talk about money everywhere – inflation, salary, investments. But want to tell you the truth? Avoiding personal finance mistakes doesn’t seem easy until we ourselves get stuck in them. I have made many mistakes too. When my first salary came, I thought the fun would begin, but in the end, only empty pockets and stress remained.

Today, in this article, we will talk about personal finance mistakes to avoid that every middle-class person ends up making. This is not just theory; it comes with real-life examples. I will explain everything in detail in about 2000 words so that you can read and think – “Oh man, I was doing this too!” Let’s get started.

Highlight key

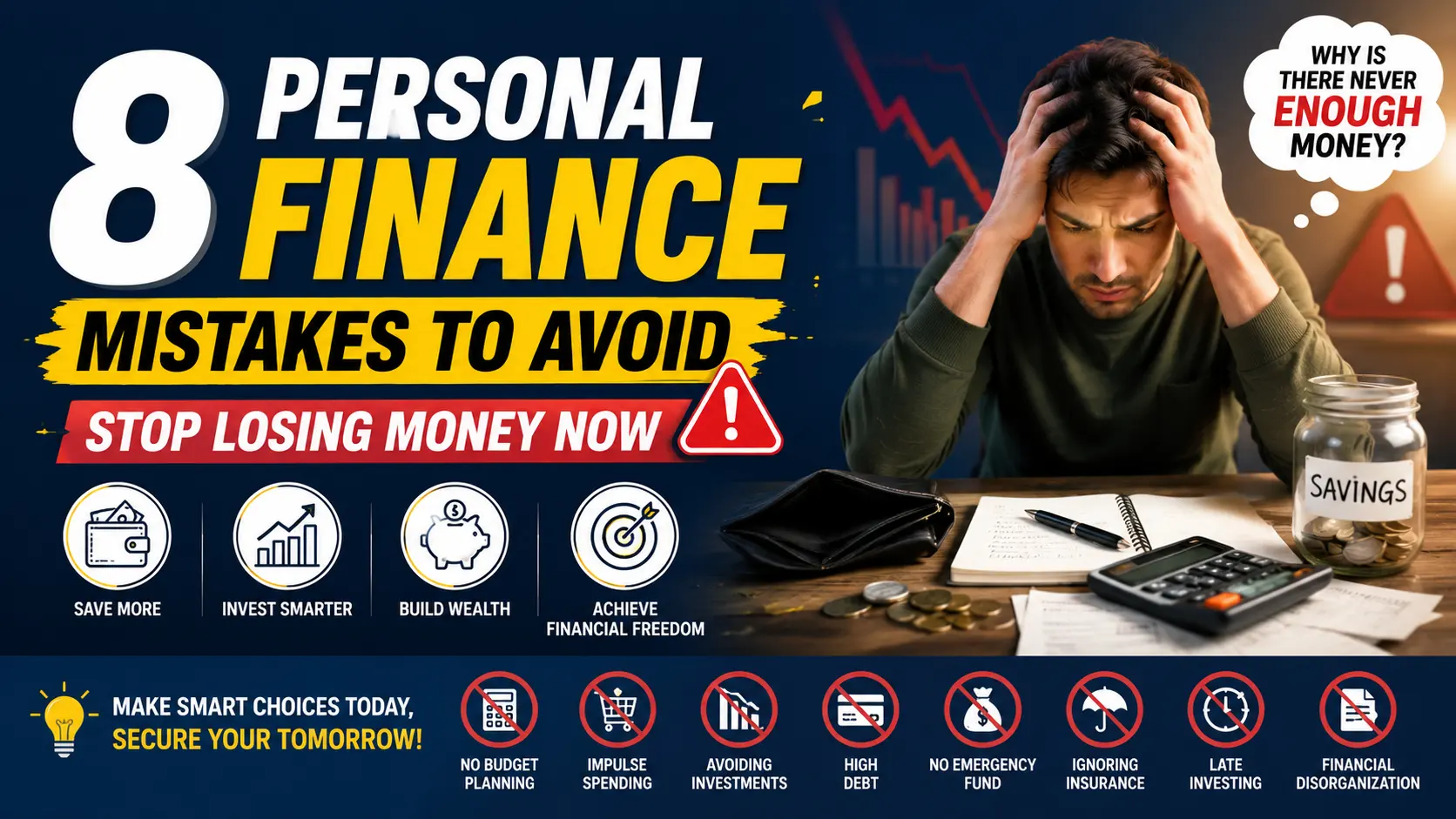

- Not making a budget – The biggest mistake, money gets lost without planning.

- Impulse Buying – Spend better in online sales, follow the 48-hour rule.

- No Emergency Fund – Save at least 6 months’ worth of expenses.

- Credit Card Debt – Don’t make minimum payments; clear the full bill.

- Lifestyle Inflation – If your salary increases, increase your savings, not your spending.

- Late Investment – Start a SIP early, take advantage of compounding.

- Wrong Insurance – Don’t just save on taxes, get term and health insurance.

- Ignore Retirement – Start planning from your 20s.

Personal Finance Mistakes to Avoid: Why Is It So Important Nowadays?

First, understand why avoiding personal finance mistakes can be life-changing. Today, the middle class in India is growing very fast, but along with that, debt and stress are also increasing. According to RBI data, credit card debt and personal loans are increasing every year. People are earning good salaries, yet still do not save money for retirement.

A friend of mine works in engineering and earns 1.2 lakh per month. Still, he borrows money every month. Why? Because he never had the mindset to avoid personal finance mistakes. Seeing such cases, I thought I should write this article so that you and your family do not have to face these problems.

Mistake 1: Completely Ignoring Making a Budget

What Are the Disadvantages of Not Making a Budget?

How to Make a Budget – Easy Tips

Use the 50-30-20 rule: 50% needs, 30% wants, 20% for the future.

Free apps on your phone, like Money View or an Excel sheet.

Review every Sunday what was spent.

This small habit is the most powerful in the list of personal finance mistakes to avoid.

Mistake 2: Impulse Buying Habit

Seeing an online sale makes you happy, doesn’t it? You fill your cart thinking, “Just this one thing.” This is also a big personal finance mistake to avoid.

Real Life Example from Varanasi

How to Control Impulse Buying?

Implement a 48-hour rule. Put whatever you feel like buying in your cart, but don’t buy it immediately. See if you still need it in two days. Minds change often. This trick saved me thousands of rupees.

Mistake 3: Not Having an Emergency Fund

Why is a 6-month fund necessary?

How to Build an Emergency Fund?

Mistake 4: Taking Credit Card Debt Lightly

The Magic of Credit Card Interest

The Way to Use Smartly

Mistake 5: Lifestyle Inflation – Salary Goes Up, Expenses Too

What Does Lifestyle Inflation Do?

How to Maintain Balance?

Mistake 6: Ignorance about investing

The Power of Compounding

Options for Beginners

- Mutual Funds SIP

- PPF, EPF

- Stock market (after a little knowledge)

- Gold ETF

Mistake 7: Thinking of Insurance Only as a Way to Save Tax

Term Plan vs Traditional Plans

Mistake 8: Treating Retirement Planning as a Doorstep

Mistake 8: Treating Retirement Planning as a Doorstep

Why is an early start best?

And Some Small and Big Mistakes That You Can Avoid

Not taking financial advice from family members

- Investing money in every scheme without research

- Focusing only on earning, not on saving

Final Words: How to Take Action Now?

Take the first step today. Grab a notebook and write down your monthly income and expenses. Then set a small emergency fund target. Start an automatic SIP every month.

Friend, I am not perfect. Even today, sometimes I indulge in impulse shopping. But after realizing these mistakes, I try to correct them. You can do it too.

If this journey of personal finance mistakes to avoid is helpful for you, share your story in the comments. What mistake did you make, and how are you improving now?

If you liked the article, be sure to share it with your friends and family. Earning money is important, but managing it is even more important.

Take care, look after yourself, and also your future.