Have you ever wondered why some people get loans so easily, and others get rejected? The answer is usually one thing: their credit score. In this guide, we will explain exactly what a credit score is, how it works in India, and how you can improve yours starting today.

Highlight key

- Credit score in India ranges from 300 to 900

- A score of 750 or above is considered good for loan approval.

- CIBIL is the most popular credit bureau in India

- Late payments and high credit usage hurt your score badly.

- You can check your CIBIL score for free once a year.

- Improving your credit score takes time, but it is 100% possible.

What Is a Credit Score? Everything You Need to Know

So let me ask you something. Have you ever applied for a loan or a credit card and got rejected, and had no idea why? I have seen this happen to so many people, and most of the time, the answer is simple: their credit score was too low.

Your credit score is basically a 3-digit number that tells banks and lenders how trustworthy you are when it comes to money.

Think of it like a report card, but instead of marks in Math or Science, it shows how well you handle your loans and bills. In India, this number ranges from 300 to 900. The higher your credit score, the better your chances of getting a loan or credit card approved fast.

Now, when we talk about credit score in India, most people mean their CIBIL score. CIBIL stands for Credit Information Bureau India Limited, and it is the most widely used credit bureau here. Banks check your CIBIL score before giving you any kind of loan or credit card.

In this article, I am going to explain everything about credit scores in simple, easy words. No confusing terms, no banker language. Just a friendly guide that actually helps you understand what is going on with your financial life.

What Does Credit Score Actually Mean?

Okay, let’s break this down properly. A credit score is a number that is calculated based on your financial history. How many loans have you taken? Did you pay your EMIs on time? Do you use too much of your credit card limit? These are the kind of things that decide your credit score.

In India, there are four main credit bureaus:

- CIBIL (TransUnion CIBIL) – the most popular one

- Experian

- EQUIFAX

- CRIF High Mark

All four give you a score between 300 and 900. Banks usually check your CIBIL score, but some lenders check Experian or EQUIFAX too.

Tell me the truth, did you even know there were four credit bureaus? Most people in India only know about CIBIL. That is totally fine because CIBIL is the most commonly used one. But knowing about the others gives you a better picture of your financial health.

Your credit score meaning, in the simplest words, means this: it tells the bank whether giving you money is a safe bet or a risky one. If your score is high, the bank trusts you. If it is low, they get worried.

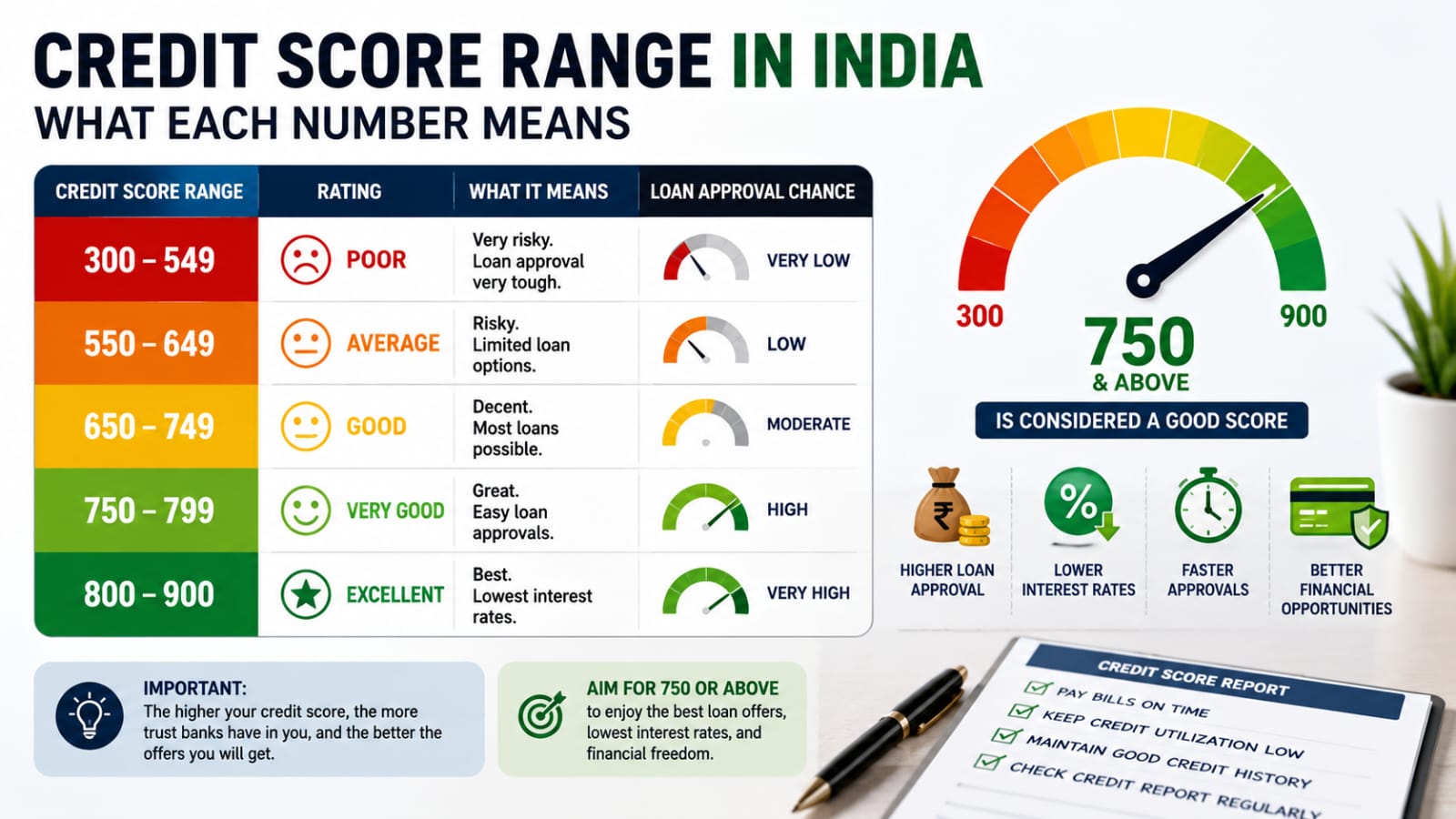

Credit Score Range India: What Each Number Means

Now, let’s talk about the credit score range in India. This is important because you need to know where you stand right now.

| Credit Score Range | Rating | What It Means |

|---|---|---|

|

300 to 549 |

Poor |

Very risky, loan approval very tough |

|

550 to 649 |

Average |

Risky, limited loan options |

|

650 to 749 |

Good |

Decent, most loans possible |

|

750 to 799 |

Very Good |

Great, easy loan approvals |

|

800 to 900 |

Excellent |

Best, lowest interest rates |

So, what is a good CIBIL score for loan approval? Most banks in India want your score to be at least 700. But if you want the best deals, low interest rates, and fast approvals, aim for 750 or above.

In my experience, people with a score above 750 get personal loan offers almost every week in their inbox and on their phones. Banks literally chase them. On the other hand, if your score is below 600, even getting a small personal loan becomes a struggle.

If you are a beginner in India just starting your financial journey, this credit score explained for beginners in India section is for you. Do not panic if your score is low right now. The good news is you can improve it. We will talk about that in detail soon.

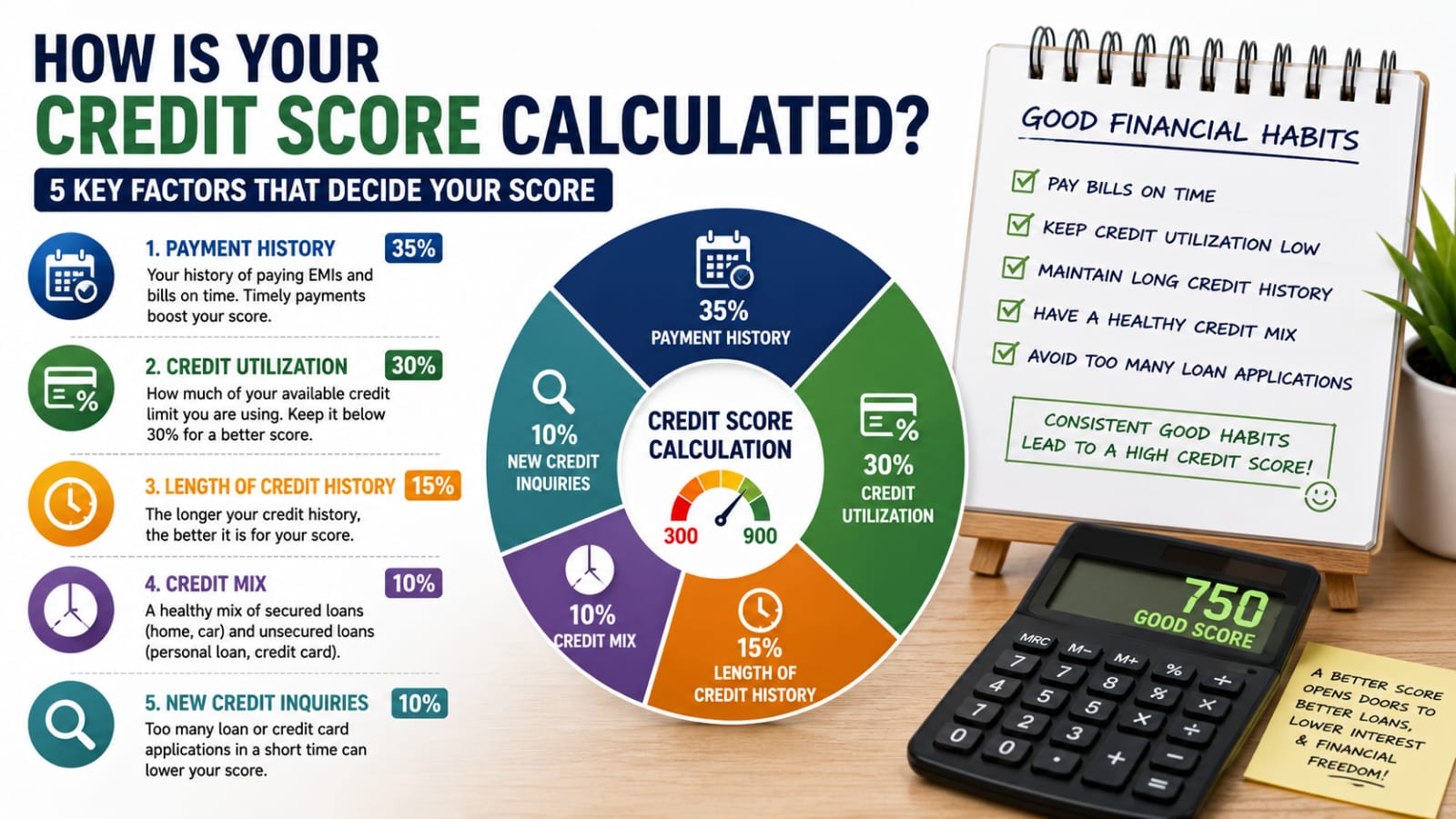

How Is Your Credit Score Calculated?

This is where it gets interesting. Your credit score does not just appear out of nowhere. It is calculated based on five main factors. Let’s go through each one.

1. Payment History (35% Weightage)

This is the biggest factor. Did you pay your EMIs and credit card bills on time? Every late payment hurts your score. Every on-time payment helps it. Simple as that.

If you think as I do, you probably forget bill due dates sometimes. I used to do that too, until I set up auto-pay for all my bills. Trust me, that one habit changed everything.

2. Credit Utilization (30% Weightage)

This means how much of your available credit limit you are actually using. If your credit card limit is Rs. 1 lakh and you regularly spend Rs. 80,000, that is 80% utilization. That is way too high. Experts say keep it below 30%.

So, if your card limit is Rs. 1 lakh, try not to spend more than Rs. 30,000 on it. This shows banks that you are not desperate for credit.

3. Length of Credit History (15% Weightage)

The longer you have had credit accounts, the better. A 5-year-old credit card with a clean history is worth more than a brand-new one. So do not close your old credit cards even if you do not use them much.

4. Credit Mix (10% Weightage)

Having a mix of secured loans (like home loans, car loan) and unsecured loans (like personal loans, credit card) is seen as healthy. It shows you can handle different types of credit.

5. New Credit Inquiries (10% Weightage)

Every time you apply for a new loan or credit card, the bank does a “hard inquiry” on your credit report. Too many hard inquiries in a short time bring your score down. So do not apply for 5 credit cards in one month, buddy.

What Is a Good Credit Score in India?

Let me be very clear here. A good credit score in India is 750 and above. If you are at 750 plus, you are in great shape. Banks will offer you lower interest rates, higher loan amounts, and faster approvals.

Now, how a credit score affects personal loan eligibility is something a lot of people ask about. Here is the honest answer:

- Score above 750: You will easily get personal loans at interest rates starting from around 10% to 12% per year

- Score between 650 and 750: You might get the loan, but at a higher interest rate, maybe 15% to 20%

- Score below 650: Most banks will reject your application, or ask for a co-applicant or collateral

- Score below 550: Very tough to get any loan from a regular bank

This is why your credit score matters so much. A bad score does not just mean rejection. It also means you end up paying more interest, even when you do get a loan approved.

How to Improve Credit Score in India Fast

Okay, now the part you have been waiting for. How to improve your credit score in India fast. Let me give you the real, practical steps that actually work.

Step 1: Always Pay Your Bills on Time

This is number one. Set reminders. Set auto-pay. Do whatever it takes to never miss a due date. Even one missed payment can drop your score by 50 to 100 points. Is it that serious?

Step 2: Keep Your Credit Utilization Low

As I mentioned earlier, stay below 30% of your credit limit. If your current spending is higher, either increase your credit limit or reduce spending. Both help your score.

Step 3: Do Not Close Old Credit Accounts

Your old credit card from 2015? Keep it. Even if you barely use it. The long credit history it gives you is valuable. Maybe use it for one small purchase every few months just to keep it active.

Step 4: Avoid Applying for Too Many Loans at Once

Every application creates a hard inquiry on your report. Multiple inquiries in a short time signal financial stress to banks. Space out your applications.

Step 5: Check Your Credit Report Regularly

Sometimes there are mistakes in your credit report. A loan that you already paid off might still show as pending. Or someone else’s loan might have been added to your report by mistake. Check it, and if you find an error, raise a dispute with CIBIL directly on their website.

Step 6: Build Credit Slowly If You Are New

If you are just starting out and have no credit history, begin with a secured credit card or a small loan. Use it responsibly and pay on time. Your score will start building over the next 6 to 12 months.

Common Mistakes That Hurt Your Credit Score

Let me share something from my own experience. A few years back, I had a friend who applied for 6 credit cards in one month because he thought it would increase his available credit. His score dropped by almost 80 points in just 30 days. He was shocked.

Here are the most common mistakes people make:

- Missing EMI payments even once

- Settling a loan for less than the full amount (this shows as “settled” on your report, which is worse than “closed”)

- Using more than 50% of your credit card limit regularly

- Closing old credit cards unnecessarily

- Co-signing or guaranteeing someone else’s loan and then not tracking if they pay on time

- Ignoring your credit report for years

Avoid these, and you are already ahead of most people.

How to Check Your CIBIL Score for Free

You can check your CIBIL score for free on the official CIBIL website once a year. You just need your PAN number, some basic details, and your email ID. The whole process takes about 5 minutes.

There are also apps and websites like Paisabazaar, BankBazaar, and others that let you check your credit score for free anytime. These are safe and do not affect your score because they do a “soft inquiry,” not a hard one.

Final Thoughts on Credit Score

Your credit score isn’t just a number; it’s a reflection of your financial habits. And the good news is, no matter where you are right now, you can improve it by following a few steps. It takes some time to see significant changes, perhaps six months or a year, but I believe it’s entirely possible.

Start small. Pay your bills on time. Use your credit cards wisely. Check your credit report once a year. These simple steps, taken consistently, will increase your credit score over time.

If you’re just starting out and have a low score or no score at all, don’t worry. Everyone starts somewhere. The important thing is to start now and stay consistent.

So, friend, take responsibility for your credit score today. Your future self, the one who gets approved for a home loan at a good interest rate, will thank you for it.

FAQ's

1. What is a credit score in simple words?

A credit score is a 3-digit number from 300 to 900 that shows banks how reliably you repay loans and credit card bills based on your past financial behavior.

2. What is a good CIBIL score for loan approval in India?

A CIBIL score of 750 or above is considered good. Most banks approve personal and home loans easily at lower interest rates for borrowers with this score.

3. How can I improve my credit score fast in India?

Pay all EMIs and bills on time, keep credit card usage below 30%, avoid multiple loan applications at once, and check your credit report regularly for any errors.

4. Does checking my own credit score reduce it?

No, checking your own credit score is a soft inquiry and does not affect your score at all. Only hard inquiries from lenders reduce it slightly.

5. How long does it take to improve a low credit score?

It usually takes 6 to 12 months of consistent good financial habits to see a noticeable improvement in your credit score, depending on how low it currently is.

6. Can I get a loan with a credit score below 600?

It is very difficult. Most banks reject applications with scores below 600. You may need a co-applicant, collateral, or to approach an NBFC with higher interest rates instead.