Highlight key

- UPI means Unified Payments Interface, a fast bank transfer system

- Works through apps like Google Pay, PhonePe, Paytm, and BHIM

- Daily limit is usually one lakh rupees for most users.

- New security rules from 2026 make it even safer.

- People in the USA can also use UPI for payments to India in some cases.

What Is UPI & How UPI Work In India

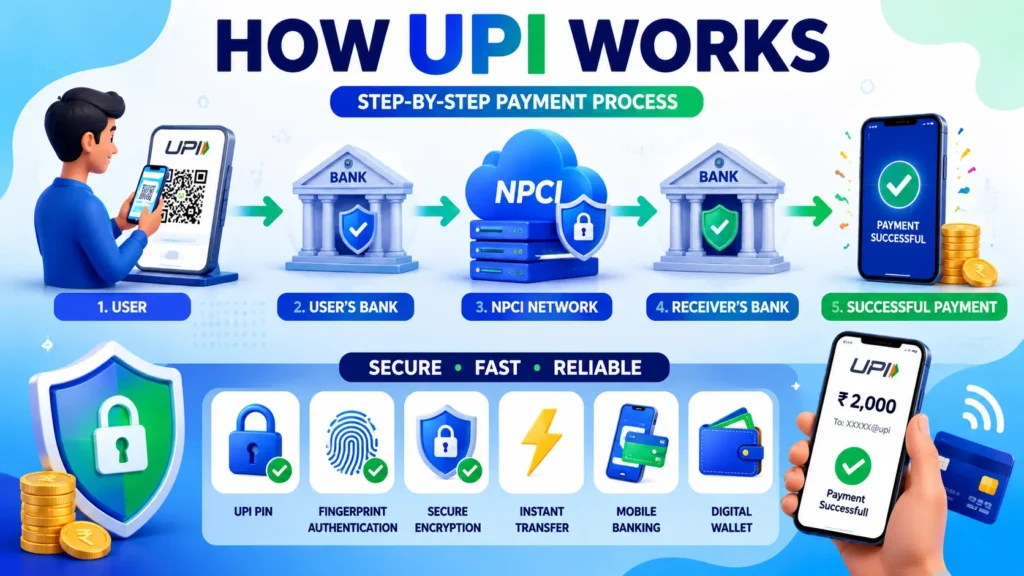

UPI is basically a bridge between your bank and another person’s bank. It works day and night, even on Sundays and holidays. In my experience, I have sent money at midnight, and it landed in seconds. No waiting, no paperwork, no branch visit.

The system links your bank account to a UPI ID or a QR code. Once you scan or enter that ID, your bank talks to the other bank directly through NPCI servers. That is the real answer to How UPI works, and it is honestly simpler than it sounds. NPCI acts like the traffic controller behind the scenes, making sure your request goes to the right bank instantly.

Tell me the truth: before UPI came along, didn’t bank transfers feel like such a headache? Long account numbers, IFSC codes, waiting for hours. Now it is just a name or number, and the money moves.

How UPI Work Step By Step

- Download a UPI app and link your bank account.

- Set a UPI PIN using your debit card details.

- Enter the receiver’s UPI ID, phone number, or scan their QR code.

- Add the amount and confirm with your UPI PIN.

- Money moves instantly between banks through the NPCI network.

Features of UPI in 2026 You Should Know

- UPI Lite for small payments without using your bank balance every time

- AutoPay for subscriptions, EMIs, and recurring bills

- Voice-based payment options for people who find typing hard

- Better fraud alerts and payee name checks before you send money

- Stronger two-factor authentication rules starting from April 2026 for extra safety

- Balance check limits, so you can check your account up to a fixed number of times daily

UPI Transaction Process and Daily Limits

The standard UPI transaction limit is one lakh rupees per day for most personal transfers. However, some categories like education, healthcare, capital markets, and government payments allow much higher limits, going up to five lakh rupees for special cases. This is helpful for salaried people and small business owners who deal with bigger amounts regularly.

If your account is new, your bank may restrict you to a smaller amount, usually around five thousand rupees for the first 24 hours. This is just a safety step, so don’t panic if you see this. Most banks also cap the number of transactions per day, often around twenty, so keep that in mind if you are making several payments in a short time.

However, it is worth noting that these limits can differ from bank to bank. Some banks are stricter, while a few private and cooperative banks allow slightly higher or lower caps based on their own risk policy.

Can People In The USA Use UPI For Payments In India

This is a common question, buddy. Right now, UPI is mainly built for Indian bank accounts. However, some NRI accounts and international UPI tie-ups are slowly expanding to countries outside India.

If you are in the USA and want to send money to family in India, apps that support UPI-linked NRI accounts can sometimes help, but it depends on your bank and app support.

Always check with your bank before assuming it will work directly, because rules can change based on your account type and residency status.

Benefits of Using UPI For Everyday Payments

- Completely free for normal person-to-person transfers

- Works for online shopping, bill payments, and small shop purchases

- No need to remember long account numbers

- Instant bank transfer at any time of the day

- Safer than carrying cash for daily needs

- Helps track your spending easily through app history

Is UPI Safe To Use in 2026

Yes, UPI is safe when used correctly. With new rules like mandatory two-factor authentication from April 2026, the system is getting stronger against fraud. However, never share your UPI PIN with anyone, and always double-check the payee name before confirming payment. That one habit alone can save you from a lot of trouble.

Therefore, it also helps to avoid clicking unknown payment links sent through messages, since scammers often use fake UPI request links to trick people into losing money.

Final Thoughts

So buddy, honestly speaking, this is pretty much How UPI works in simple terms. It’s fast, mostly free, and gets more secure every year with new NPCI and RBI rules.

Whether you’re using it daily in India or trying to figure it out to send money to your family in the US, this cashless payment system is going to get even bigger in a few years. Stay updated, watch out for your PIN, and enjoy the convenience it offers.

Disclaimer:

This article is for educational and informational purposes only and should not be considered financial, banking, investment, or legal advice. UPI transaction limits, security features, bank policies, and RBI/NPCI guidelines may change over time and can vary by bank or payment app. Always verify the latest information with your bank, the official UPI app, or relevant authorities before making financial decisions or high-value transactions. Never share your UPI PIN, OTP, or banking credentials with anyone, and use digital payment services at your own risk.